Rentokil

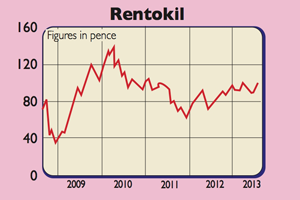

I tipped Rentokil (LSE: RTO) as a buy at 89p at the start of July. I did so because I thought the shares were cheap on 10.5 times forward earnings, which undervalued some very good businesses within the company. Having got rid of the troublesome and loss-making City Link parcels business, I had hoped that the market would begin to focus on this fact.

Quite a bit has happened in the last few weeks. Alan Brown, the current chief executive, has announced that he is leaving. Meanwhile, the company has delivered a reassuring set of half-year results. The shares have bounced nicely to 103p, which now rates the company on a higher forward price/earnings multiple of 12.1 times. A quick gain of 15.7% on the shares is nice to have – but I think there’s more to go for with Rentokil.

First and foremost, I believe there’s room for a new chief executive to make further improvements to the business. Now that City Link has gone, he can finish tidying up the company by getting rid of the facilities management business which does things like catering, cleaning and security for the government and commercial customers. It doesn’t make a lot of money and has much lower margins than the rest of the business.

This would leave Rentokil with three good businesses – pest control, hygiene and workwear – with high profit margins and good returns on capital employed (ROCE). These businesses have decent prospects despite tough trading in Europe. The company has also been buying up similar businesses in fast-growing emerging markets, which makes a lot of sense.

The new boss will be under pressure to boost the profits of these businesses. Despite its good financial performance, many investors think that Rentokil should be doing better than it is. There’s always the chance that a management team from another company might think they could do a better job, and so attempt to buy Rentokil outright. If the facilities management business is sold, it makes for a cleaner purchase. That said, even ignoring potential bid hopes, City analysts still expect earnings growth of 11% next year and increased cost savings could see this rise. The shares still look worth buying.

Verdict: keep buying

Darty

Electrical retailer Darty (LSE: DRTY) has done well since I tipped it in March at 41.75p. The shares have soared by 77% to 73.75p at the time of writing and have been as high as 82p. The rationale for buying Darty is that it is a distressed investment. Selling electricals is a cut-throat business, especially when you have to compete against the likes of Amazon. As Darty has found out, trying to build a pan-European business in this market has been foolhardy.

Yet Darty has three decent businesses, in France, Belgium and the Netherlands. It has got out of Italy and shut all its shops in Spain. If it can get out of Turkey, the Czech Republic and Slovakia, then it will have a profitable business that could still look cheap at the current share price. But recent trading has been weak, with product margins under pressure and debt edging up. So it’s tempting to take profits.

But there are a few things that might keep you on board. The new chief executive, Regis Schultz, previously turned around French furniture retailer But, and could do a similar job here. Along with the chairman, he has just bought £200,000 worth of Darty shares. Also, activist shareholder Knight Vinke has a 25% stake, which it bought at over 100p, and it also has a seat on the board. Will it really want to sell out at a loss?

Darty is also still a contrarian investment, with only one out of the 14 analysts covering the stock rating the shares a buy. It will only take one or two of these to turn positive to see the shares spike up again. Despite the temptation to cash in, I think Darty shares are still an interesting gamble.

Verdict: hold on to your shares