“The next few months promise to be particularly tricky and volatile for markets,” says Pimco’s Mohamed El-Erian in the Financial Times. The jittery political backdrop, with military action in the Middle East, Germany’s upcoming election on 22 September, and Italy’s coalition hitting trouble again, doesn’t help. But the main threat stems from central banks.

The attempt to drain all the liquidity they have flooded the markets with in recent years (through quantitative easing, or QE) is fraught with risk. “Wall Street is showing itself loath to give up QE3, even gradually,” says Randall W Forsyth in Barron’s. Hints from Federal Reserve chairman Ben Bernanke that the Fed will merely seek to buy fewer assets with printed money – as opposed to stopping QE altogether – have still sent both stocks and bonds lower.

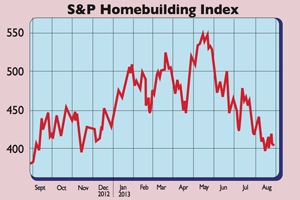

More seriously, bond yields have rebounded around the world due to talk of ‘tapering’ QE. That could dampen global growth, which is already slow, says Ed Yardeni of Yardeni Research. For instance, the bounce in US mortgage yields “is depressing mortgage applications, both to refinance and to purchase a home”. The US house-building sector scents trouble: it has fallen into a bear market since tapering talk began in May.

In Britain, higher mortgage rates, thanks to higher gilt yields, imply further damage to the housing market and banks’ balance sheets, says MoneyWeek’s Tim Price in his Price Report. Talk of less QE has also “created a sense of panic” in emerging markets, says James Mackintosh in the FT. The flood of money tempted into riskier assets by central-bank cash is reversing. The resulting instability dampens growth prospects in emerging economies.

Meanwhile, it isn’t proving easy for central bankers to talk yields back down again, especially in the UK: markets are sceptical of the Bank of England’s intention to keep interest rates low for three years despite inflation being above target. Central banks, says Richard Barley in The Wall Street Journal, may be losing control of global bond markets.

Investor scepticism will only mount if higher rates threaten the world economy to such an extent that central banks panic and throw yet more QE at the markets, which in turn will fuel fears of worse inflation further down the line. The great money-printing experiment is looking less and less likely to end well.

• Stay up to date with MoneyWeek: Follow us on Twitter, Facebook and Google+