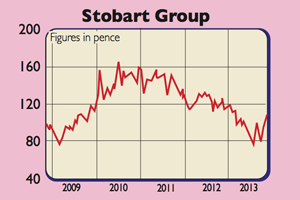

Stobart Group (LSE: STOB)

I tipped shares in the Stobart Group as a gamble back in December at 95p. For most of the time since, the company has endured a lot of turmoil. A profit warning earlier in the year dented confidence while in-fighting among the directors has done the company’s reputation with investors no good at all – the previous chairman lasted only ten weeks. But there’s hope that, with a new person in the role, Stobart is a happier ship now.

The company is best known for its distinctive trucks that plough up and down Britain’s motorways. The trucking company is a reasonable business that manages to eke out a reasonable living in very tough markets. A legacy property business is gradually being sold off to pay down debt. However, it is the potential of Stobart’s ownership of Southend airport that keeps me interested in the shares. I think that this asset has huge potential to make lots of money for its shareholders, as it has a lot of good things going for it.

The main terminal extension is nearly finished and the airport has excellent car parking facilities and decent rail links. It has also just won the Which? airport of the year award for its high levels of customer satisfaction. EasyJet, the airport’s main customer, is doing well. It has just added a fourth aircraft to the airport while announcing some new destinations. This should see passenger numbers at the airport grow by 20%.

Airport capacity in the southeast of England is hard to come by, which is good news for Southend. Also, as passengers can get in and out of the airport quickly, it wouldn’t surprise me if some airlines begin to see Southend as a viable and cheaper alternative to using nearby Stansted. EasyJet is clearly expanding its business here and others could follow.

Given that Stobart has put a lot of money into the airport, it looks well placed to start getting a growing stream of cash flow back. Regional airports have proven to be decent investments in the recent past and have realised very high prices. Growing traffic at Southend could see this reflected in Stobart’s share price in the years ahead. The 6p dividend looks like it will be maintained for the time being, meaning that investors are being paid to wait.

Verdict: keep buying at 111p

Aga Rangemaster (LSE: AGA)

Aga shares have done well – up by 55% – since I tipped them as a very risky buy last December. With trading subdued and a massive pension fund deficit that could wipe out any value in the shares, I figured that things were pretty bad. Aga could double if trading picked up, or just as easily go bankrupt.

Chancellor George Osborne has come to the rescue with his Help-to-Buy scheme, aimed at boosting the UK housing market. If recent history is anything to go by, a rising housing market is good for sales of the very expensive, but very well made Aga and Rangemaster cookers.

So it’s no surprise to hear that Aga orders were up by 8% during the first six months of 2013, while demand for Rangemasters – which have been popular in new-build houses in the past – is starting to pick up after a slow start. When Help to Buy is extended to the whole housing market next April, I expect Aga could be in for a further sales boost.

The company is now pinning its hopes on its new electric Agas and wants to see existing customers trade up to better models. If they do, Aga’s profits could soar, given that it has very high fixed costs (or operational gearing), which would see a large chunk of any extra sales from new cookers turn into profits.

Aga’s pension fund liabilities are still an issue. The fund will get its hands on any extra cash before shareholders do. But higher bond yields in recent months have meant the problem isn’t getting any worse.

With the housing market steaming ahead, Aga shares may have further to run.

Verdict: keep buying at 113p

• Stay up to date with MoneyWeek: Follow us on Twitter, Facebook and Google+