In the late 1980s Japan’s potential growth rate was estimated at around 4% by the Bank of Japan. These days the economy’s speed limit is thought to be less than 1%.

That’s for three main reasons: the working-age population is shrinking; companies have slashed investing after years of stagnation; and productivity has dwindled.

Japan’s prime minister, Shinzo Abe, is now trying to tackle this with a package of reforms aimed at boosting productivity and, ultimately, growth. This is the so-called ‘Third Arrow’ of his programme to end years of deflation (the first two were money printing and more government spending).

Some have criticised the reforms as too timid. But as one former US official told Reuters, it’s unrealistic to expect an attempt to overcome all of the economy’s vested interests in one go. “It isn’t a Big Bang”, but it is a lot better than previous reform packages that failed. The reforms are likely to produce “less than Abe hopes but more than sceptics expect”, says David Pilling in the Financial Times.

The government plans to cut corporation tax from 35% to below 30%. It will loosen up the labour market by allowing firms to negotiate pay and conditions directly with staff, and will get rid of a spousal tax benefit that has discouraged women from working. It also wants to end monopolies in the utilities sector and free up the inefficient agriculture sector.

Meanwhile, it is working on improving corporate governance via the new JPX-Nikkei 400 stock index, which government pension funds are being encouraged to invest in. The government also plans to expand a foreign trainee programme – which may be a tentative first step to boosting immigration to offset the shrinking native workforce.

Much depends on whether the government delivers. But if it can, says JPMorgan’s Jesper Koll, the economy’s potential growth rate could rise from 0.8% a year now to 1.5% in the medium term. The Bank of Japan is also ready to print more money to reach its inflation target of 2%, which it currently looks like missing.

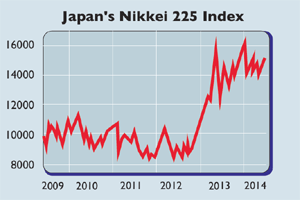

The economy is recovering from April’s hike in the consumption tax, and companies look cheap. According to Morgan Stanley, the market’s forward p/e hasn’t been this low compared to its developed-market counterparts for 20 years. Japan remains a buy.