This Midlands metal basher is a throwback to the days when companies just got on with their own business and spent little time wooing the suits in the City.

For over 50 years, the maker of castings that end up in big heavy trucks has been under the influence of executive chairman Brian Cooke – by all accounts a no-nonsense kind of man who apparently prefers paper records to computers and doesn’t like talking to the City that much.

There’s a lot to like about this ‘what you see is what you get’ approach. The company also has a reputation for being very prudent with its accounts, which is always welcome. However, when it comes to investing, it all boils down to whether a company is any good at serving its customers and if you can buy its shares for the right price.

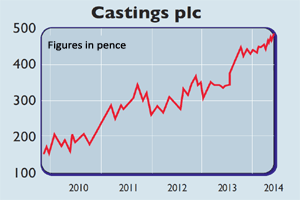

Castings (LSE: CGS) has staged a remarkable recovery since the dark days of the last recession. Back then, demand for heavy trucks nosedived and with it the orders for Castings’ products. Having slashed the workforce by a third in order to remain competitive, the company is once again in rude health.

That said, Castings remains a risky business for investors. It’s very good at what it does, but the demand for trucks tends to fluctuate a lot, depending on the economy. For Castings, this primarily means the European economy, which has been struggling for some time now. The other factor is the increasing clampdown on emissions from truck engines. This has been very helpful recently as a new standard (known as Euro 6) introduced this year saw a surge in orders for late model trucks before it was introduced.

Manufacturing companies such as Castings have a lot of fixed costs – bills that have to be paid whether the foundries are running at full capacity or have plenty of slack. This means that their profits are very sensitive to small changes in sales levels.

Castings grew its profits nicely last year as it had lots of work to do. This year is a little less easy to predict as orders from truck makers have slowed down a bit. However, Castings expects demand to pick up in the autumn and winter months. The strength of the pound is another concern.

The shares have done well over the last couple of years and are certainly not depressed, trading on just over 12 times next year’s earnings. However, despite some uncertainties, I expect Castings’ profits to benefit from a recovering European economy, which means its shares could still go higher over the next few years.

Verdict: buy at 472p