US company profits beat expectations in the second quarter of 2014. Companies in the S&P 500 index grew earnings per share (EPS) by 8.4% on average – the best quarterly showing in three years.

But dig a bit deeper and the profit picture isn’t as robust as it looks. And this is true not just of the recent quarter, but of the entire post-crisis profit rebound.

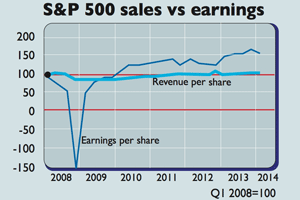

For a start, healthy earnings growth doesn’t reflect the underlying economy. Sales (revenue) growth has been very weak, as the chart shows. Instead, the boost to earnings has come partly from historically high profit margins, which in turn have been helped greatly by sluggish wage growth.

However, firms have also exploited another way to boost EPS – they have been buying back their own shares. Buybacks raise EPS by reducing the number of outstanding shares.

Buybacks can boost share prices, as some investors see them as a sign that a stock is cheap – why would management buy the stock otherwise? As Michael Mackenzie notes in the Financial Times, since the start of 2013, a US exchange-traded fund (ETF) that tracks firms doing buybacks has beaten the S&P by a third.

But “a less charitable view” is that management is out of ideas for investing to grow the business. There’s also the fact that buybacks can boost managers’ bonus payments by giving EPS – a key performance measure – an artificial lift.

But can it continue? In 2013, buybacks worth a record $671bn, or 3.9% of US GDP, were announced. This year around $300bn or so of shares will be repurchased. That’s more than four times the amount retail and institutional investors have put into equity funds.

The first quarter of 2014 marked the peak of the buyback wave, with $160bn announced, compared to $120bn in the second quarter.

Why is the momentum ebbing? Many companies have taken advantage of record-low interest rates, fuelled by quantitative easing (QE), to borrow money to fund buybacks. But QE ends in October, while net debt in the American corporate sector now stands at a record $2.3trn, up 14% in the past year.

So, there seems little scope for the buyback boom to keep going. “When it finally sputters, be prepared for it to weigh on forward earnings expectations,” says Chris Versace on Foxbusiness.com. The bull market, in short, looks set to lose one of its drivers.