Whichever way you look at it, a car will usually cost you a lot of money over the years. And brand new cars are money pits. The rate at which they lose value (‘depreciate’) in the first three years of life is truly frightening, and very bad for your wallet.

Sure, I can see the appeal – no hassle, all the latest gadgets – but if you buy a new car, you need to realise that you’re paying a hell of a big price for the luxury of doing so.

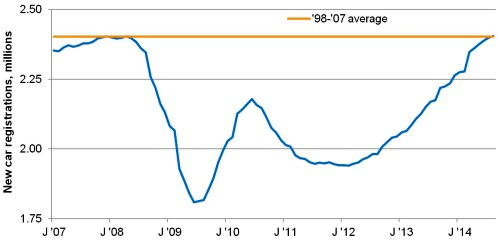

Yet it seems I’m in a minority. Britain’s new car market – as with the housing market – is booming. New car registrations are back to pre-recession levels (see chart below) and have been growing for the last two and a half years. Private buyers who might have bought a second-hand car in the past are now buying new ones.

UK new car registrations (rolling years)

Source: SMMT

How are cash-strapped consumers paying for all this? After all, the economy may be recovering, but we keep hearing that wages haven’t kept up.

One factor is that the banks’ bad habit of conning their customers has left many people with considerable windfalls due to the mis-selling of payment protection insurance. That’s created plenty of money for deposits.

But as with many of the UK’s problems, the main factor is something all too familiar – easy credit. You see, British car buyers – and sellers – have discovered the wonders of PCPs (personal contract purchases) in their droves. This type of finance is paying for around seven out of ten new cars bought in Britain today.

PCPs are a very clever way for car manufacturers and dealers to sell more cars, as they make it very easy for people to buy. Instead of getting a loan or hire purchase (HP) agreement to buy the car, you effectively agree to rent the car for a period ranging from 18 months to four years. A PCP essentially has three parts to it:

• An upfront cash payment

• A series of monthly payments (typically over three years)

• An optional final payment based on a guaranteed future value for the car (based on things like annual mileage)

As you are not paying off the whole purchase price of the car, the monthly payments under PCP are lower than with a personal loan or HP agreement. This explains why consumers like them so much.

But what happens after the three-year PCP is up? You either have to buy the car, or hand it back and get a new one with another PCP – but you can only do that if you can find another source of cash to fund the deal. And despite banks’ persistent mis-selling, there’s only so much PPI money left to go round.

So ‘rolling over’ these PCPs might be easier said than done. In fact, I think PCP has created a false picture of the health of the UK car market. To keep car sales at current levels, dealers and manufacturers are reliant on this scheme to keep going.

Here’s how I think they are doing it: I changed the family estate car last week (I bought a two-year old one), but on my two visits to the dealership, this is the sort of conversation I overheard quite a few times:

“Hi, Mr Jones. Yes, we can get you a new one of those in a few weeks – you’ll only be paying £2 more a month than you are already.”

I was curious about what was going on. So I began trawling some of the many car forums on the internet. As I thought, it seems that quite a few people on PCPs are being offered the opportunity to trade in early, and roll over to a new deal. Dealers and manufacturers have sales targets to be met – and this is a good way of doing it.

But this credit-fuelled car bubble looks very dodgy to me. If consumers can’t find the cash for a new deal, or interest rates rise (driving up rental payments) it will all come crashing down.

Some tips for getting a good deal on a second hand car

Yet it could have a silver lining if you are on the lookout for a newer motor. You see, it won’t be long before the used-car market could be flooded with ex-PCP cars that have reached the end of their contract. This would cause second-hand values to fall sharply. Better yet, it’s more likely than not that these cars will have both low mileage and a main dealer service history, and so could be excellent buys. There’s no VAT to pay, and a large chunk of the depreciation period has already passed.

To see why buying a car second hand is generally much better value than buying new, you just have to look at the chart below. It shows the rate of depreciation on Britain’s most popular car, the Ford Fiesta. A top-end petrol model costing £13,545 brand new will be worth just £5,375 after three years – less than 40% of its original value. That’s £227 of depreciation per month.

Depreciation of a 5-dr Ford Fiesta Zetec 1.25L 82bhp

Source:Whatcar.com

So let’s say you’ve spotted a three-year old model Ford Fiesta that you like. It might be on a dealer’s forecourt for £6,500. How do you go about getting a good deal?

Do your research. That gives you the evidence you need to haggle convincingly. Websites such as Cap or Parkers are excellent for finding out what prices cars should sell for, and what the trade-in value of your car should be.

You could even do some maths yourself. Selling used cars can be very profitable for dealers, and many will look to make margins of around 12%, according to industry sources. So, the Ford Fiesta with a depreciated value of £5,375 should sell for no more than £6,100 (to give a profit margin of 12%), assuming not much preparation work has been needed.

But don’t get too fixated on the selling price. Focus on the cost to change (the difference between the price of the car and the value you can get for your trade-in vehicle). Work out what your own maximum cost to change is before you visit the dealer, and be prepared to walk away if you can’t achieve it.

Also try and find out how long the car has been up for sale. Dealers need to turn cars into cash fast. Providing there’s nothing strange about the car, one that’s been on the forecourt a while might be able to be had for a chunky discount.

In short, while a shiny new car may seem tempting, I’d resist – the market for used cars might just be about to become a lot more favourable for savvy buyers.