Have you ever fancied working at the top of a tall building? Perhaps not. But people in that position want peace of mind that if they should slip or fall, then there will be something in place to make sure they don’t come to any harm.

This is the bread and butter of this Wiltshire- based company, which makes specialist workplace safety kit. It has been going through a bit of a hard time over the last couple of years. Weak European economies have meant that construction companies haven’t been busy and haven’t bought a lot of its kit.

On Tuesday this week, Latchways (LSE: LTC) announced that things had got even worse. Wind-farm projects in Europe have been delayed, while a key American customer has apparently got too many of Latchways’ products and doesn’t need to order as many this year.

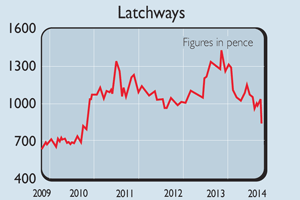

Despite places such as the UK and Latin America doing better, pre-tax profits for the year to March 2015 are expected to be between £4.5m and £5.5m, compared to £6.8m last year. The shares were duly hammered and fell by 17%. Investors were probably wishing that there was a bit of safety kit to keep the shares from falling further.

Yet Latchways’ management insists that this is a temporary blip and that the future will be much brighter. The directors have pledged to maintain last year’s 39.5p dividend and hope that the 4.8% yield will persuade people to be patient. On top of this, there’s more than £10m of cash in the bank and no debt – in other words, there’s no risk of the company getting into financial difficulties.

Let’s just hope that the directors were right when they said that the blip was temporary. After all, they said similar things in June when they announced that profits had fallen from nearly £11m the year before. That said, on closer inspection Latchways looks like a quality business, even when things aren’t going too well.

For example, on profits of just £4.5m it would still be making a return on capital employed of 18%, which is pretty decent. Two years ago, that figure would have been over 40% – not many companies are capable of that.

Latchways’ shares were over £14 back in November last year and don’t look like returning to those levels anytime soon. However, if you believe the management when it says that profits can rebound strongly over the next couple of years, then the shares could be a good buy for contrarian investors.

Verdict: a buy for the brave at 830p