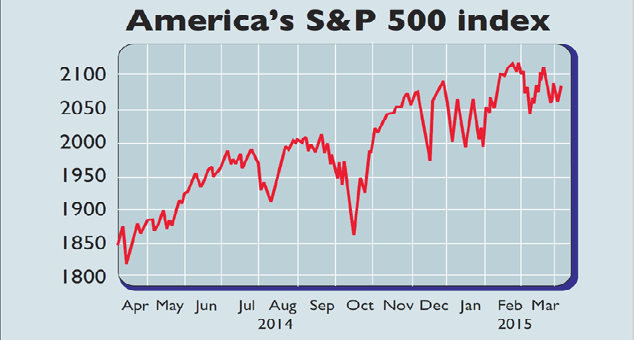

“Staying bullish on US equities has become a lot harder,” say Nicole Bullock and Eric Platt in the FT. The S&P 500 has delivered a 250% return – including reinvested dividends – in the six years since March 2009. But a key tailwind is fading, says Buttonwood in The Economist. Profits bounced back to record levels after the global financial crisis, yet now they are weakening. Earnings per share climbed at an annual rate of almost 8% in the fourth quarter. But they are expected to rise by a mere 2.6% in 2015. And estimates for the first quarter of this year have been revised downwards at the fastest rate since 2009. Earnings are projected to have declined by 5% on an annual basis between January and March.

One reason for this is the stronger dollar, which reduces multinationals’ foreign profits when converted back into greenbacks. Lacklustre growth in emerging markets and Europe’s slow recovery aren’t helping either. Meanwhile, the plummeting oil price also undermines sales because the energy sector comprises around 10% of the index.

Investors have also noticed that large US firms have relied on cost-cutting and buybacks to spur earnings growth in recent years. With margins at record highs, there is scant scope for squeezing out cost reductions, especially with a tighter labour market implying higher salaries. So boosting revenues has become all the more important. Yet with the economy having softened slightly in recent weeks, that looks unlikely for now. Indeed, sales are expected to slide by almost 3% in the first quarter.

Given the approaching headwind from higher interest rates, “there will need to be ‘real’ growth in earnings and top-line revenue for equities to move higher from here”, says Oliver Pursche of Bruderman Brothers. Valuations also look far too high, making the market vulnerable to a setback. The cyclically adjusted price/earnings (Cape) ratio is 68% above its long-term average.

Even on a rolling forward p/e basis – taking the next 12 months’ earnings-per-share estimates – the p/e is 17.4. Beyond a brief foray above this level in 2004, it has only been higher in 1998-2003, says Longview Economics. That period marked the tech bubble and subsequent collapse. No wonder investors are leaving America for Europe and Japan while the S&P has barely budged his year.