George Osborne’s new tax rules will almost certainly make residential property in the UK less attractive to investors. But do certain areas have more potential than others? The UK housing market is often referred to as a bubble market, and affordability is certainly not improving, with average wages lagging house-price growth. However, if you take a step back from the UK-wide averages, then there’s a very clear divide between north and south – or more explicitly, between London and everywhere else.

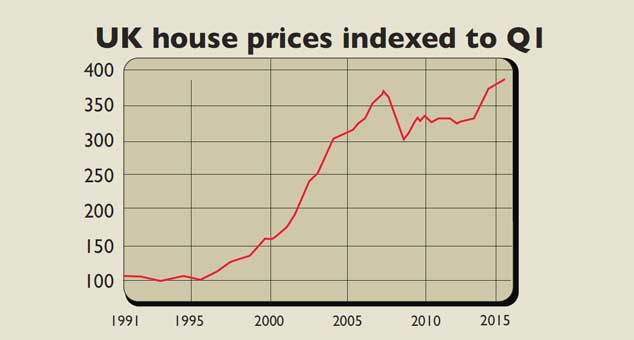

If you look at Nationwide’s price data, for example, then even in nominal terms (ie, ignoring inflation, which would make the figures look even worse), house prices in many areas are still lower than they were at the peak of the last bubble. In Northern Ireland, average house prices are still more than 40% down on the peak. The region has been battered by the fallout from Ireland’s bubble, so it arguably should be excluded for these purposes. But prices in Scotland, Wales and the north of England are 5%-8% lower than in mid-2007 (a pretty

grim return over eight years). In the Midlands, prices are flat. In the South West, prices are up about 5%, while

in East Anglia they are 7% higher.

Of course, certain towns and cities will have done better or worse than others – it’s hard to generalise across whole nations, as for Scotland and Wales. But for “mania” conditions, there’s no question that London and its commuter belt in the South East are the only regions where we’re genuinely back to post-crash bubble territory. London prices are roughly 40% higher than at the 2007 peak, with a 20% rise in the “outer metropolitan” area (the bits that are within commuting distance of London) and a 13% rise in the rest of the South East.

And according to an analysis of Land Registry data by The Guardian, London is by far the least-affordable area, with the average property price now 12 times the regional average income – compared to 4.4 times in 1995 (which was also high by UK standards at the time). We’re not suggesting you pile into buy-to-let – now that the government has landlords in its sights, the latest tax raid is unlikely to be the last. But if you do, the figures suggest you should look beyond London.

Now’s not the time to start up as a landlord

Peer-to-peer property-lending platform LendInvest has built a buy-to-let index based on sales and rental data from property website Zoopla. The index suggests that the best areas to own a buy-to-let property – in terms of pure yield, rather than including capital gains (which, naturally, are highest in London) – include Glasgow (with double-digit yields apparently available in both the city centre and some outlying areas), Peterborough and Liverpool.

Make of all that what you will. The truth is that if you want to invest sensibly in buy-to-let property, what matters – as with any sensible investment – is the income that it’ll produce for you over time. You can’t bet on capital growth materialising (as many investors, happy with miniscule yields in the likes of London, seem to be doing right now), particularly given that – as James notes above – it’s hard to see interest rates going lower from current levels, even if it takes a while for them to rise again. And therefore, the key point about the chancellor’s changes to the buy-to-let tax regime is that they will make it harder to get a decent yield on buy-to-let, across the board. That has to make it less attractive as an asset class overall.

If you’re still dead keen, remember that – again, as with any other asset class – your yield should reflect your risk. LendInvest’s buy-to-let index might indicate double-digit yields in less salubrious areas of Glasgow, but that’s because they’re riskier bets than a waterfront flat in central London. And if, on the other hand, you can only muster up a single-digit yield, are you really better with a single buy-to-let property than a portfolio of blue-chip dividend-paying stocks? In all, given the alternatives, it’s hard to make the case for buy-to-let right now – now is not the time to start a career as an amateur landlord.

See also:

The death knell for buy-to-let?

Record low interest rates have been a boon for a generation of private landlords. But the party’s coming to an end, says James Ferguson. The death knell for buy-to-let?.