Bond-market liquidity “sounds like a pretty niche subject”, as The Daily Telegraph’s Ben Wright puts it. Yet it has many people’s “knickers in a twist”. Why? It seems that – as usual – regulators’ response to the last crisis may have sown the seeds for the next. Liquidity refers to both the size of a market (how many buyers and sellers there are) and its depth (how many buyers and sellers of small and large amounts of securities are available). In bond markets, banks have traditionally acted as market makers, matching buyers with sellers, or buying big chunks of bonds themselves in anticipation of selling later. They have thus “smoothed out temporary mismatches” in the market, says Wright.

But now, rules to make banks safer have made it pricier for banks to hold bonds – so they are increasingly reluctant to do so. So now, “market depth is far lower than it was prior to the Lehman crisis”, notes CrossBorder Capital. The total inventory of US Treasuries available to market makers today is roughly $1.7trn, from $2.7trn in 2007. Yet the overall market is far bigger – worth $13trn, up from $4.5trn in 2007. In corporate-debt markets, too, there is much less liquidity to grease the wheels. According to Deutsche Bank, the amount of US corporate debt outstanding has doubled since 2001, but dealer inventories are down 90%.

A sudden lurch downwards?

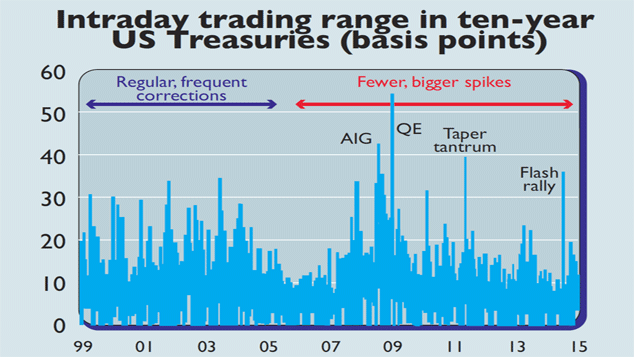

Worse still, bond markets are eye-wateringly expensive at a time when interest rates are expected to rise, which implies lower bond prices. The worry, then, is that the lack of liquidity could see a sell-off turn into a rout, with prices tumbling as everyone tries to sell, and very few market makers are there to buy. That would see yields soar, raising debt payments across the economy, and tearing holes in financial institutions’ balance sheets. A dearth of liquidity, in other words, could cause the next crisis. There have already been some violent, and statistically rare lurches in the US Treasury market, notably last October’s “flash rally” and the “taper tantrum” over the withdrawal of quantitative easing (see chart).

Meanwhile, the yields on interest-rate swaps (derivatives used by companies to manage their interest-rate exposure) have slipped below those on short-term US Treasuries. That’s illogical – investment banks are the counterparties in the swaps market, so swaps being more expensive than the underlying bonds “suggests that governments are less creditworthy than the very financial institutions they bailed out”, says Bloomberg.com. Again, this seems at least partly due to new rules, which have prompted banks to switch bonds for swaps because they are cheaper and exempt from tough capital requirements. Nobody is certain of the cause, but as Thomas Urano of Sage Advisory Services says, the fear is there is something big “brewing under the surface that so far hasn’t been pinpointed”.