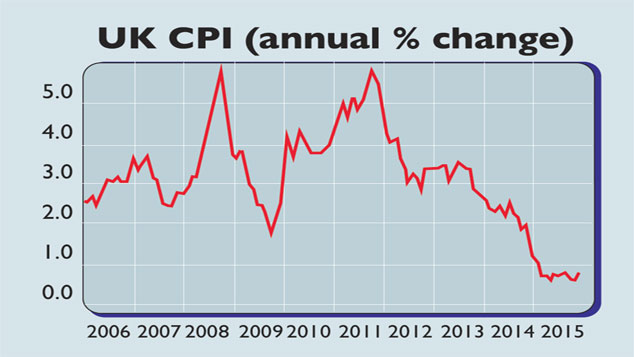

Inflation has edged back above zero. The annual increase in the consumer price index (CPI) climbed to 0.1% in November, from -0.1% the month before. Underlying inflation, stripping out volatile food and energy costs, ticked up to 1.2%. Meanwhile, employment rose further in the three months to September, taking the employment rate to a record high of 73.9%, and lowering the unemployment rate to another post-crisis low of 5.2%. The pre-crisis low was 4.7%, reached in 2005. But the claimant count measure of unemployment ticked up, and annual pay growth eased to 2.4% in October, from 3% in September.

What the commentators said

2016 is likely to see “an end to deflation but continued lowflation”, as Citi’s Michael Saunders put it. There is scant sign of pricing pressure in the pipeline: factory gate prices slid by 1.5% year-on-year last month, a tad faster than October’s decline. Oil prices have slid sharply again recently and wages are now rising less quickly. Throw in the Bank of England’s 2% CPI target, and an interest-rate hike seems unlikely anytime soon. The Bank “will wait until a sustained pick-up in wage growth is evident”,

said Martin Beck of the EY Item Club. That could take “some time”.

But perhaps not as long as the market thinks, said Capital Economics: its forward projections of interest rates imply no movement from the Bank until 2017. But overall inflation, even if oil prices stay stable at $40, would be back above 1% by next September as the much bigger falls of 2014 passes out of the annual comparison. Imported goods price inflation should climb too as the impact of sterling’s recent strength ebbs. Meanwhile, there are signs that productivity is finally beginning to rise, which implies higher pay.

The weekly wage growth data is stronger than it looks, according to Pantheon Macroeconomics. It has been skewed of late by a slight dip in average weekly hours worked to 32. The Centre for Economics and Business Research, moreover, thinks the national living-wage policy could soon push earnings growth back up to an annual 3%. That in turn is set to fuel a 3% real increase in inflation-adjusted household spending, the key driver of growth. So the hawks at the bank “could soon have something to get their teeth into”, said FT.com. The upshot? Capital Economics and Pantheon Macroeconomics are both pencilling in the first rate rise for the second quarter of 2016.