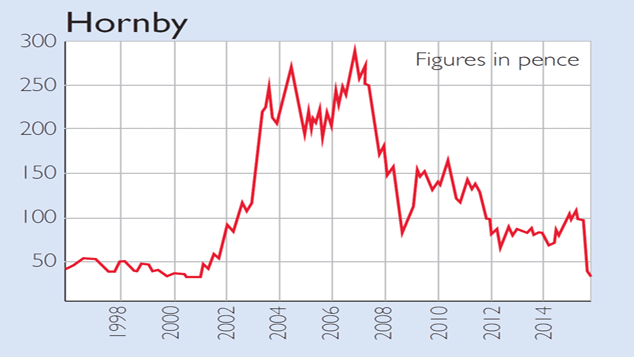

Hornby’s model trains remain a firm favourite for nostalgic baby boomers, looking for something to tinker with beyond their pensions. But with the shares at a 15-year low, should investors pile into the stock?

Hornby (LSE: HRN), one of Britain’s oldest and best-loved brands, is facing the possibility of foreclosure this month, as the company negotiates with lenders over £9m of debt. The Kent-based firm, which makes toy trains, Airfix, Scalextric and Corgi cars, had a good Christmas. But an update in February said sales have collapsed since, leading to the worst day for Hornby’s shares since it floated in 1986. The company is on course to lose £5m to £6m this year and is at risk of breaching debt covenants with its lender, Barclays. Hornby is in talks with the bank and its chief executive has stepped down, replaced by the chairman, Roger Canham.

The firm was founded by Frank Hornby, a clerk in Liverpool who also invented Meccano, and has been making trains out of steel rather than plastic since the 1920s. But in 1999 it shifted production to China and has faced inventory problems ever since. Suppliers have moved factories, delaying new lines from hitting the shelves. Hornby has also struggled to keep a handle on its supply chain, stretching from China to WHSmith, forcing it to upgrade its stock management system and leading to a £1m write-down last month, after a stock-take at its warehouse in Kent.

That is a lot of missing wagons. But management has the power to increase cash flow and margins in the UK, says Ruffer’s fund manager Alex Grispos, one of Hornby’s biggest investors. Its blunder has been chasing higher sales in Europe, while trying to streamline the business: a target that was “too ambitious” for an iconic but low-growth brand.

The much-loved brand has survived several previous bankruptcies and buyouts, changing hands in the 1960s, 1970s and 1980s. It is unlikely to disappear completely from British shelves. But its chances of surviving in its current form look increasingly slim. Buy the trains, not the shares.

Three to buy…

Victoria

The Mail on Sunday

Carpet-maker Victoria was founded in Scotland in 1895 and made the red carpet for Prince William’s wedding. The shares have rocketed as the chairman, Geoff Wilding, a former investment banker from New Zealand, has cut costs and made canny acquisitions. Victoria is now the biggest carpet-maker in the UK and the second biggest in Australia. Wilding is “on a mission”, says The Mail on Sunday. His plans have “further to go”.

Cineworld

Investors Chronicle

Massive blockbusters last year, including Spectre and Star Wars, pushed up ticket sales at cinema chain Cineworld to a record £94m. Earnings and dividends have both jumped and the company will struggle to beat its performance in 2016. But growth in eastern Europe should provide a shot in the arm.

STV

Shares

Shares in Scottish broadcaster STV slumped 18% last week and are trading under ten times earnings. But the government is making noises about introducing retransmission fees, charging pay-to-view channels such as Virgin and Sky to carry free channels, like the BBC. That should be a boon for ITV and STV, pushing the sector higher.

… and three to sell

Aldermore

The Times

Aldermore is a challenger bank, alongside Metro and Virgin Money, says The Times. But in reality, it’s more like an old-fashioned building society. It takes deposits from investors and lends them out at a higher rate. Growth looks likely to be stunted and it is difficult to see what will boost the shares.

Foxtons

The Daily Telegraph

Foxtons has built its business around London’s house-price boom, but don’t rush to buy after its latest drop in profits. London’s property market is growing sluggish and oversupplied. Transaction volumes are down and residential sales fell 10% last year. Competition is also fierce.

And the rest

.basic-table {

border-spacing: 0px;

border-collapse: collapse;

border: 1px solid #a6a6c9;

font-family: Calibri, Verdana, Helvetica, sans-serif;

font-size: 1em;

color: #000000;

width: 100%;

}

/* same as basic-table but with smaller font */

.basic-table-small {

border-spacing: 0px;

border: 1px solid #a6a6c9;

font-family: Calibri, Verdana, Helvetica, sans-serif;

font-size: 0.8em;

color: #000000;

width: 100%;

}

/*table with no border – use btfirst for leftmost cells */

.noborder {

border-spacing: 0px;

border-collapse: collapse;

border: 0;

font-family: Calibri, Verdana, Helvetica, sans-serif;

font-size: 1em;

color: #000000;

width: 100%;

}

/* headers */

th.bth, th.headnorm {

background: #2b1083;

padding: 3px 3px;

border-left: 1px solid #a6a6c9;

border-bottom: 0;

border-right: 0;

border-top: 0;

color: white;

font-weight: bold;

text-align: center;

}

/* normal cells – left aligned, and centered */

.btfirst {

padding: 3px 3px;

border: 0;

vertical-align: center;

text-align: left;

}

td.btleft {

padding: 3px 3px;

border-left: 1px solid #a6a6c9;

border-right: 0;

border-top: 0;

border-bottom: 0;

vertical-align: center;

text-align: left;

}

td.btcenter {

padding: 3px 3px;

border-left: 1px solid #a6a6c9;

border-right: 0;

border-top: 0;

border-bottom: 0;

vertical-align: center;

text-align: center;

}

/* row shading */

tr:nth-child(even) {

background: #ffffff;

}

tr:nth-child(odd) {

background-color: #E1E8F4;}

}

/* “naked” version (no vertical border and bigger, serif font) */

.basic-table-naked {

border-spacing: 0px;

border: 0px;

font-family: font-family: Georgia, Times, ‘Times New Roman’, serif;;

color: #000000;

width: 100%;

}

th.bth-naked {

background: #fff;

padding: 8px 3px;

border: 0px;

font-size: 1.1em;

font-weight: bold;

text-align: left;

vertical-align: center;

}

td.btleftnaked {

padding: 3px 3px;

border: 0px;

vertical-align: center;

font-size: 1.1em;

text-align: left;

}

td.btcenternaked {

padding: 3px 3px;

border: 0px;

vertical-align: center;

font-size: 1.1em;

text-align: center;

}

| Buys | |

|---|---|

| Aviva | The insurer has surplus cash and the shares are yielding 5% (Times) £4.66 |

| Breedon Aggregates | Breedon is growing quickly through targeted bolt-on deals (Times) 68p |

| Charles Taylor | The firm has “sticky” clients and is cheap since a rights issue (Inv. Chron.) £2.45 |

| Greggs | Greggs is investing in its supply chain; earnings should rise (Shares) £11.26 |

| John Laing | It’s infrastructure deals make the shares a “safe haven” (Times) £2.19 |

| Lancashire | Key team members have been leaving, but the 9% yield is tempting (Shares) £5.32 |

| McCarthy & Stone | Sales are rising quickly at the retirement home builder (Shares) £2.48 |

| Robert Walters | Asia is now a profit centre for the recruiter and profits are up (Inv. Chron.) £3.15 |

| Whitbread | Sales dips have hurt the shares – buy now they’re cheap (Inv. Chronicle) £37.30 |

| Sells | |

| 4imprint | The printer’s shares have risen sharply; bank some profits (Mail on Sunday) £12.70 |

| Amec Foster Wheeler | The dividend has been trimmed and assets sales are likely (Times) £4.78 |

| B&M European | The discount retailer is seeing softer sales and strong competition (Shares) £2.89 |