Welcome back. I was on holiday, now Merryn’s on holiday, so no new podcast this week I’m afraid. (But a note for those of you who were listening to our experimental podcast Money Minute – it will be returning soon in an exciting new format – more on that later this month.)

That said, if you’re in Edinburgh this month and you’d like to hear the closest thing to the podcast live, then pop along to Panmure House for a salon with Dominic Frisby (until 16 August) or Merryn (from 17 August) and their guests (which will include me on the 22nd and 23rd). Book your ticket here – last year it was a lot of fun and there’s even more stuff to talk about this year.

If you missed any of this week’s Money Mornings, here are the links you need:

Monday: The return of the trade war sparks panic in markets

Tuesday: China fires a warning shot as the trade war escalates

Wednesday: A beginner’s guide to Adam Smith, part I

Thursday: Are trade wars rattling markets, or is it fear of another blow-up in Europe?

Friday: The bullish and bearish cases for oil prices

Currency Corner:A frustrating lesson in trend-following from the US dollar

Subscribe: Get your first six issues of MoneyWeek free here

And if you’re looking for some holiday reading, I will not-so-humbly suggest my book on contrarianism, The Sceptical Investor. And if you’ve already read it, please leave a review on Amazon if you feel so inclined – it’s always nice to get feedback.

Now, to the charts. I’ve been away for the last two weeks, so inevitably, all the exciting stuff has happened in my absence. The one caveat I’d put in all of this is that it’s August, so there is a faint sense of unreality about everything. Everyone gets back into work/back-to-school mode in September and that’s when we get to see which trends have staying power and which were just brief summer panics. But for now it certainly feels as though something significant has changed.

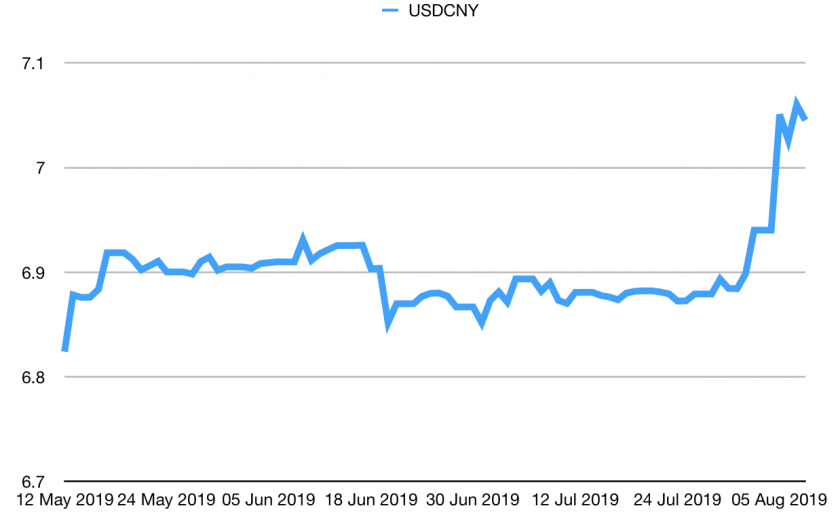

Let’s shake it up a bit this week – we’ll turn first to the number of Chinese yuan (or renminbi) you can get to the US dollar (USDCNY). Why is this our priority this week? Because this week it breached the critical ¥7.0 level that we (and everyone else) has viewed as a line in the sand.

For more than a decade, China has made sure that the yuan hasn’t weakened beyond this point. This week, it stopped doing that; mainly because the US is putting is under more tariff pressure. Tariffs increase the prices of Chinese exports to the US, but if the yuan weakens against the US dollar, this offsets the tariffs.

China is also making a political point. The yuan is certainly a manipulated currency, but China has mostly intervened in recent times to keep it strong (not weak, as the Trump administration argues). By letting the yuan slip through this key threshold, the message is clear – the gloves are coming off, and we’re prepared to devalue further if the trade disputes continue.

Why does that matter? Put simply, if yuan devaluation picks up pace and becomes “disorderly”, as the pundits put it, then that could hurt the Chinese economy and be deflationary (capital flight tends to spread chaos), not to mention the drop in the price of Chinese exports all around the world, which would also be deflationary. Deflation is the big bogeyman of the day, so markets wouldn’t like that.

For now, China seems to be in control of the exchange rate but it’s a big advance in the currency wars.

(Chinese yuan to the US dollar: three months)

The irony is that this mostly stems from the Federal Reserve’s failure to act as aggressively as markets had hoped at its last interest-rate setting meeting. The Fed cut by a quarter point and didn’t sound dovish enough. So both markets and Donald Trump threw a hissy fit.

I suspect we’ll see more aggressive action by the Fed at the next meeting, because for a moment there, Jerome Powell looked as though he could breathe a sigh of relief. Prior to the meeting, the yield curve had been looking healthier than it had for months.

(A quick reminder of what the yield curve is – it’s the difference (“spread”) between what it costs the US government to borrow money over ten years and what it costs over two years. You can use other borrowing periods, and many do, but this is arguably the most important one. Once this number turns negative, the yield curve has inverted, which almost always signals a recession, although perhaps not for up to two years.)

The curve between the three-month and the ten-year had even “un-inverted” the last time we looked at it, in the third week of July.

Unfortunately, that all changed after the Fed. The three-month curve is inverted again, and now as the chart below shows, the gap between the two-year and ten-year (which hasn’t yet gone negative in this cycle) is looking decidedly queasy. If that doesn’t turn up soon, it’s as good a confirmation of pending recession as we’re likely to get, I think.

(The gap between the yield on the ten-year US Treasury and that on the two-year, going back three months)

Gold (measured in dollar terms) had a stellar week (which I suspect will please a lot of readers). There are a fair few reasons for this but one is that in a world of negative nominal interest rates (ie, where you have to pay to lend money, or to store fiat currency with a risk-free government), then gold carries no opportunity cost, and may in fact offer you more chance of preserving your capital (bearing in mind that gold is very volatile on a day-to-day basis).

(Gold: three months)

The US dollar index – a measure of the strength of the dollar against a basket of the currencies of its major trading partners – has rallied strongly in recent weeks. This week was more subdued (partly because everyone was buying the Japanese yen and Swiss franc, the ultimate “haven” currencies) but it’s too soon to tell if the world will get any relief from the strong dollar.

(DXY: three months)

Ten-year yields on major developed-market bonds have cratered, to put it lightly, amid fears of recession and a rush for “safe” assets.

Below we see the US ten-year Treasury yield:

(Ten-year US Treasury yield: three months)

And then there’s Japan:

(Ten-year Japanese government bond yield: three months)

And finally, Germany, plumbing fresh lows amid dreadful economic data:

(Ten-year Bund yield: three months)

Copper rebounded a little after a rough couple of weeks, after Chinese export data came in a little bit better than expected (an unexpected recovery in Chinese growth is probably one of the things that could drag the global economy back from the brink, at least sentiment-wise).

(Copper: three months)

The Aussie dollar rallied, after crashing hard over the last couple of weeks.

(Aussie dollar vs US dollar exchange rate: three months)

Meanwhile cryptocurrency bitcoin has had a good run and it does look more and more as though people are starting to classify it (in their heads and portfolios at least) as a peculiar alternative to gold.

(Bitcoin: ten days)

Despite all the concerns about a slowdown, US jobless data is still holding up well. US weekly jobless claims came in at just 209,000, lower than expected, while the four-week moving average edged a little higher to 212,250.

US stocks typically don’t peak until after this four-week moving average has hit a low for the cycle, and a recession tends to follow about a year later (remember that this is not scientific – it’s a tiny sample size, originally highlighted by David Rosenberg at Gluskin Sheff). The last low came about three months ago, at around 201,000.

So it’s not inconceivable that we could see a fresh low set, although that does rather clash with a lot of the other gloomy data out there right now.

(US jobless claims, four-week moving average: since January 2016)

The oil price (as measured by Brent crude, the international/European benchmark) has slid hard in recent weeks as sentiment has turned and demand growth figures have looked weak.

(Brent crude oil: three months)

Internet giant Amazon, the stock you won’t get fired for owning, fell then recovered along with the wider stock market this week.

(Amazon: three months)

It was a similar story for electric car company Tesla.

(Tesla: three months)

That’s us for this week – but just before I go… by 22 November , we’ll have a lot more clarity on all of these topics, from recession to trade and currency wars and, of course, the impact of Brexit.

That would make it the ideal time to be able to hear views from a wide range of experts discussing all of those topics and how they might affect your portfolio, and perhaps even have a drink with some of those experts after they’ve had their say.

But where might you find such a gathering of top minds? As luck would have it, I have the solution for you right here – they’ll all be at the MoneyWeek Wealth Summit, in central London. Book your ticket now – it could be the best financial decision you make all year.