Quick thing – very exciting announcement to make about the Wealth Summit – we’ve got Dylan Grice, formerly of Societe Generale, now of Calderwood Capital, joining our panel on The Future of Money.

Dylan has long been one of the most interesting thinkers in the investment world – don’t miss the chance to see him in conversation. Get your ticket here now.

We’ve also got a fantastic investment trust panel lined up – Sebastion Lyon of Personal Assets Trust, Simon Elliott of Winterflood and Dan Whitestone of Throgmorton will be giving Merryn their views on everything from the investment outlook to a certain fund manager’s downfall.

That’s just a tiny sample of what we’ve got planned for the day. And we haven’t even announced all the guests yet. Seriously, you’ll be kicking yourself if you miss it – Get your ticket here now.

Podcasts, Money Morning, Currency Corner and Merryn’s blog

On the podcast front, Merryn and I finally recorded a new one this week. In fact, we had to record it twice. On Wednesday, we were talking about what might happen to Woodford Patient Capital if another manager took it on. The next morning, Schroders promptly did just that, stealing our thunder somewhat. Here’s the Friday afternoon version, where we ponder whether Patient Capital is now a ‘buy’ or not.

If you missed any of this week’s Money Mornings, here are the links you need:

Monday: Another Brexit delay – so what happens now?

Tuesday: Markets are getting over their burst of summer panic – but why?

Wednesday: The future of money is borderless – and difficult to tax

Thursday: A beginner’s guide to gold: what’s it for?

Friday: Is it time to buy Patient Capital Trust?

Currency Corner: What’s next for the mighty US dollar?

Subscribe: Get your first 12 issues of MoneyWeek for £12

Deal: get 25% off a copy of my book, The Sceptical Investor

And don’t miss Merryn’s blog on the demise of cash machines.

The charts that matter

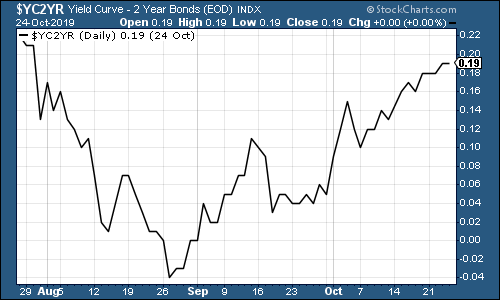

The yield curve

edged further into positive territory this week (in other words, the yield on the ten-year US government bond is higher than the yield on the two-year, which is how things should be). The curve inverted about two months ago, which usually indicates that a recession is on the way within 18-24 months. We’ll see if it holds true this time (I have no reason to doubt the indicator, but these things are rarely 100% accurate).

(The gap between the yield on the ten-year US Treasury and that on the two-year, going back three months)

Gold (measured in dollar terms) had a largely uneventful week, drifting sideways.

(Gold: three months)

Similarly to gold, the US dollar index – a measure of the strength of the dollar against a basket of the currencies of its major trading partners – was little changed. Right now it seems to be grinding higher in the long run, as hat’s next for the mighty US dollar?

(DXY: three months)

The number of Chinese yuan (or renminbi) you can get to the US dollar (USDCNY) edged lower.

(Chinese yuan to the US dollar: three months)

Yields on ten-year yields on major developed-market bonds were little changed on the week.

The US ten-year was basically flat on last week.

(Ten-year US Treasury yield: three months)

As was Japan…

(Ten-year Japanese government bond yield: three months)

And Germany.

(Ten-year Bund yield: three months)

The price of copper perked up amid concerns that social unrest in Chile will hit supply – Chile is one of the world’s most important copper producers.

(Copper: three months)

The Aussie dollar was little changed on last week.

(Aussie dollar vs US dollar exchange rate: three months)

Cryptocurrency bitcoin had another bumpy week – the price tumbled on Wednesday then perked right back up on Friday.

(Bitcoin: ten days)

US weekly jobless claims fell back this week to 212,000, a bit lower than expected, from 218,000 (revised up from 214,000) last week. The four-week moving average came in at 215,000.

A sustained uptrend would indicate that a recession is close. We’re not there yet, but it’ll be interesting to see what the US nonfarm payrolls – due on Friday – reveals.

(US jobless claims, four-week moving average: since January 2016)

The oil price (as measured by Brent crude, the international/European benchmark), edged higher this week.

(Brent crude oil: three months)

Internet giant Amazon’s share price fell somewhat this week after third-quarter earnings missed expectations. But initial falls were tempered because as usual with Amazon, it’s because Jeff Bezos was spending lots of money making the group even harder compete with, by expanding the company’s same-day delivery service.

(Amazon: three months)

Meanwhile shares in electric car group Tesla surged this week as investors applauded the company’s third quarter results. The company actually made a profit (analysts had expected a loss) and said that its Chinese factory is running ahead of schedule.

(Tesla: three months)

Have a great weekend. Hope to see you on 22 November!