The UK energy regulator Ofgem has warned again that tightening electricity supplies could cause blackouts by 2015. One new solution is the government’s Green Deal initiative. This incentivises families to install new energy-saving appliances (boilers, insulation, etc) to reduce power consumption and carbon emissions.

Last week the first scheme was announced by Birmingham City Council. And the firm it chose as its exclusive outsourcing partner under an eight-year, £600m deal was Carillion.

Initially the scheme will cover up to 60,000 households across the city, together with schools and other council properties. Another £900m framework contract allows 35 neighboring councils to buy similar services from Carillion. Other regions such as Southampton and Newcastle are also pushing ahead with similar schemes, and Carillion looks well placed to become the ‘go-to’ provider.

The firm’s overall strategy is to build up its support-services arm – which maintains roads, railways and other essential infrastructure – while shrinking its lower-margin, UK construction business. Earlier this year the group signed one of the largest local authority contracts of its kind – a £700m agreement to provide services ranging from property management to school catering and cleaning for Oxford county council over ten years.

CEO Richard Howson says the public sector continues to outsource services to improve operational efficiency, which in turn underpins the firm’s record £35.6bn pipeline. The firm is bidding on five local-authority contracts this year and is also in pole position to win a £1.5bn contract for the upkeep of the Ministry of Defence’s airfields, army bases and naval sites. And outside of the UK, the board is aiming to double revenue from the Middle East and Canada by 2015.

First-half operating margins rose to 4.1% from 3.3% despite sales slipping. The order book held up well too at nearly four years’ sales.

Carillion (LSE: CLLN), rated a BUY by Panmure Gordon

The City is forecasting sales and underlying earnings per share (EPS) of £4.6bn and 41.8p respectively, climbing to £4.8bn and 42.1p by 2013. That puts the shares on a mean price/earnings (p/e) of seven, with a well-covered 5.8% dividend yield. I value the stock on a ten times EBITA multiple. Adjusted for the £163m PFI portfolio, debt of £284m, minority interests, and a £248m pension deficit, that suggests a fair value of 370p a share.

The next update is scheduled for 12 December. Panmure Gordon has a price target of 400p.

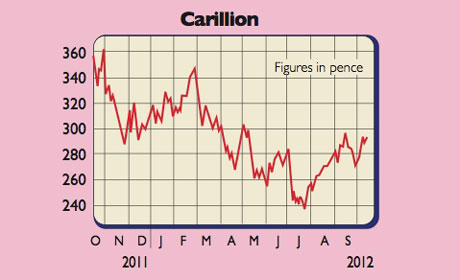

Rating: BUY at 287p

Disclosure: I own shares in Carillion.

• Paul Hill also writes a weekly share-tipping newsletter, Precision Guided Investments. See www.moneyweek.com/PGI or phone 020-7633 3634.