“Light at last,” says Pierre Briancon on Breakingviews. The EU has finally fleshed out the terms under which it will give a bail out if Greece requests one. The EU would extend up to €30bn of loans for three years at an interest rate of just over 5%, while the International Monetary Fund will provide another €15bn at a cheaper rate. This amounts to around 20% of Greece’s GDP.

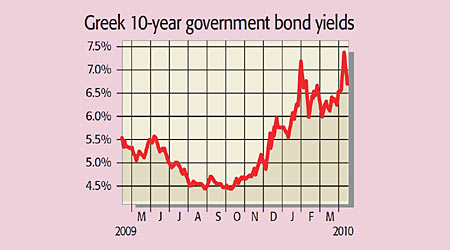

The deal sent the euro to a three-week high, lowered Greek bond yields and helped ensure a successful auction of Greek short-term debt on Tuesday. Last week, the worry was that Greece would soon be unable to meet its short-term financing needs as demand for its debt had dwindled and yields soared.

The package is a short-term fix that should help Greece meet its financing needs for the next few months, but it’s not a long-term solution. Greece hopes to carry out “monumental fiscal tightening even as it slides deeper into recession”, says David Owen of Jefferies. They risk “chasing their tail”.

The interest rate on the EU loans is higher than “any realistic assessment” of Greek growth over the next few years, says Sean O’Grady in The Independent. So they won’t make a dent in their huge debt pile, which is only likely to grow as austerity blows further holes in the budget and hence also raises the interest burden. So the likely scenarios are either a vicious debt spiral, or default, because the cuts prove “politically impossible” to deliver.

No country has ever fixed a major hole in its finances without either a devaluation (not possible for Greece as it is in the euro) or a default, says Christopher Swann on Breakingviews. “It’s hard to believe” that Greece will become the first to do so.