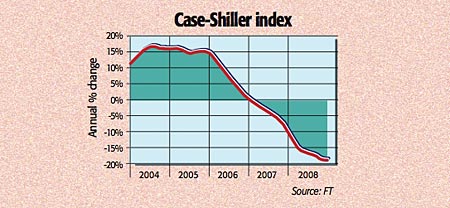

It’s just as well that Barack Obama’s first speech to Congress wasn’t an official state-of-the-union address, said Economist.com. The union’s state is “awfully precarious”. The consumer confidence index has collapsed to a record low and, according to the S&P/ Case-Shiller index, house prices slid by 18% in the three months to December – a record annual decline. They are now 27% off their bubble peak.

Downtrend is far from over

With the overhang of unsold homes still at near-record levels, prices still have some way to fall, implying further consumer retrenchment. Already, for the first time since the 1940s, consumer spending, which comprises around 70% of GDP, has fallen by an annual rate of over 3.5% for two consecutive quarters, said Bloomberg.com. GDP slid at an annualised rate of about 5% in the fourth quarter and Ben Bernanke, the chairman of the Federal Reserve, said the economy would only recover from the “severe contraction” if policy makers can stabilise the financial system. But the system is far from stabilised.

Insurance giant AIG, already 80% owned by the state, is now expected to unveil a $60bn loss for its most recent quarter as “it picks through the wreckage” of insurance contracts it wrote on dodgy mortgage and commercial real-estate derivatives, said Stephen Foley in The Independent. It is hoping for another cash infusion, while Citigroup has also been seeking further help.

Regulators are now embarking on “stress tests” of banks’ capital positions and will issue more preferred shares that can be converted to common equity when losses materialise.

What next for banks?

A key aim of this “fiddlyness” is to avoid “the appearance of nationalisation”, said Economist.com; the Citigroup deal apparently calls for any government stake to be capped at 40%. Yet the plan “is another step towards taking control” of the biggest banks, said Lex in the FT. This may be a political hot potato in the US, but temporary state ownership is the “only option that would permit us to solve the problem of toxic assets in an orderly fashion and finally allow lending to resume”, said Nouriel Roubini in The Washington Post.

Banks have been loath to mark down their assets and take losses because they have been hoping that their value would recover, while a high government price for bad debts would amount to a subsidy for banks – and thus give taxpayers a raw deal. Full state ownership would align the interest of taxpayers and banks, and by forcing banks to mark down their assets to market would reveal who is bust and who isn’t. The insolvent banks would be recapitalised and then returned to the private sector.

The alternative, keeping “a series of de-facto insolvent banks on long-term life support”, as Josh Marshall on Talkingpointsmemo.com. put it, looks costlier in the long run. It’s time to “bite the bullet”.